Articles of Interest

A Plan Sponsor Guide to Climate Aligned Investment Approaches

The impact of climate risk remains a priority for investors as many environmental changes now have a larger and longer impact. Climate changes will continue to translate into market risk as policymakers receive more pressure to preserve environmental progress and retool economies in a more sustainable manner. To combat the impact of climate risk, a growing number of Canadian plan sponsors and administrators are assessing their portfolios and working to define and adopt an active approach to decarbonization consistent with their long-term investment objectives.

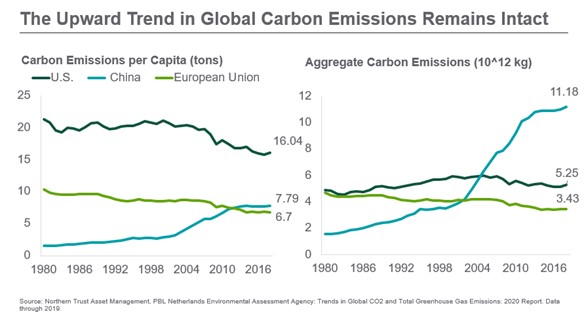

Global carbon emissions rose despite the brief respite caused by lockdowns. As governments prepare to meet at the UN Climate Change Conference of the Parties COP 26 in November, many are drafting new regulations to combat this challenge. Central banks globally are also seeking solutions. The Network for Greening the Financial System, a collaborative initiative which includes the Bank of Canada, recognized that climate change poses a systemic risk to the global economy. The European Central Bank is now addressing how it will include climate risk in its monetary policy. In the United States, the Federal Reserve’s Board of Governors created two entities, the Financial Stability Climate Committee, and the Supervision Climate Committee, that are tasked with oversight on the broad financial system and individual institutions, respectively.

Source: Northern Trust Asset Management, PBL Netherlands Environmental Assessment Agency: Trends in Global CO2 and Total Greenhouse Emissions:2020 Report. Data through 2019.

Climate risk could negatively impact economic growth, inflation and investment returns. In order to analyze the impacts, we differentiate between two types of climate risk: physical risk and transition risk. Physical risk is the amount of damage to land, buildings or infrastructure that is caused by droughts, storms and flooding. Transition risk is the impact to businesses or assets that arises from policy, legal and market changes as transitions are made to a lower-carbon producing economy.

The biggest threat climate change poses to financial markets is the impact to equity returns. Natural resource and emerging market stocks are the most vulnerable. Fragile economies in emerging markets could be more sensitive to climate-related regulation since they are still in early stages of maturation and often produce higher carbon emissions.

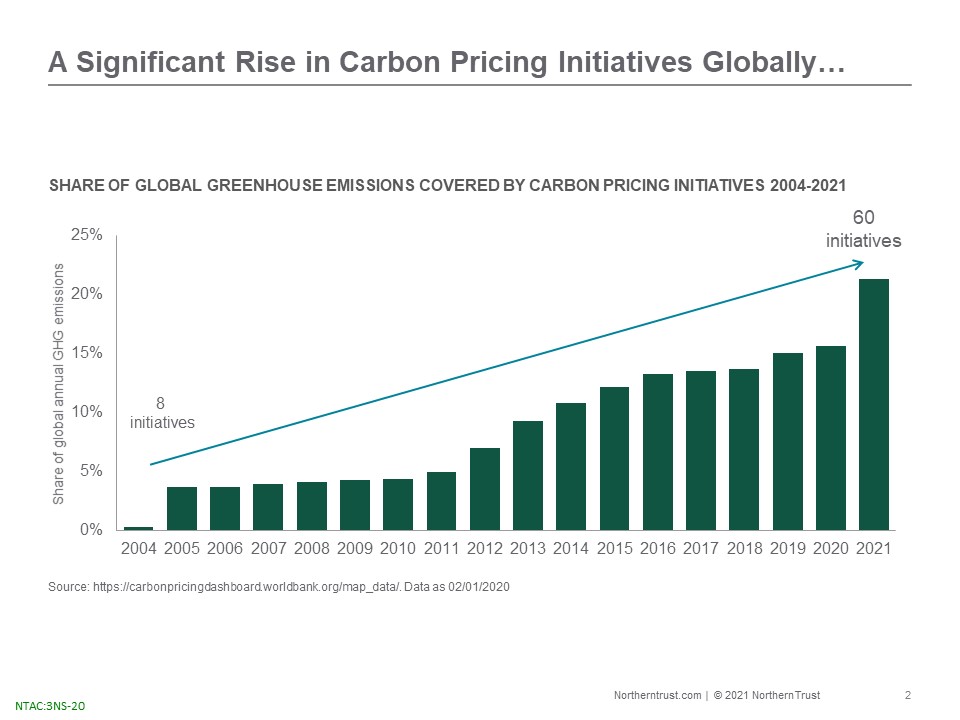

Investors could view climate risk with more urgency since the pandemic demonstrated how large non-financial events can impact returns. Investors should seek to avoid the repricing that is likely to occur. Since 2019 every jurisdiction in Canada developed a price on carbon pollution due to initiatives that were established. One way for investors to circumvent repricing is to focus on the portfolio construction process.

Source: https://carbonpricingdashboard.worldbank.org/map_data/. Data as 02/01/2020

Asset owners have a variety of tools and frameworks available to incorporate climate risks into the portfolio construction process. These assessments rely on disclosures from investee companies as well as research by third parties. Northern Trust Asset Management supports the recommendations of the Financial Stability Board’s Taskforce on Climate-Related Financial Disclosures (TCFD), which includes the disclosure of governance structure overseeing climate-related risks, the risks themselves that analyzed under different climate scenarios, strategy and efforts to manage them, as well as the list of targets and metrics used.

In 2019 Canada’s Expert Panel on Sustainable Finance released its final report establishing recommendations to support the growth of sustainable finance in Canada, including a recommendation to develop a Canadian Stewardship Code to address how fiduciaries should account for climate risks and other material ESG issues. Institutional investors in the Canadian markets have acknowledged this threat. In 2020, the Responsible Investment Association (RIA) reported C$3.2 trillion assets were managed in sustainable strategies across the Canadian market, a 48% uptick compared to the report two years earlier.[1] Climate change was identified as a main driver of adoption of sustainable investing in the region and dominated the list of factors that investors consider in previous trends reports. The upward trend in adoption of this approach is clear, but there are several pathways that investors take in the implementation process. Plan sponsors should note that pension funds represent roughly half of the assets represented in the 2020 RIA report, driven largely by 10 sizeable public pensions with commitments to investing sustainably. In addition to large institutions, individual investor appetite, particularly younger investors, has been noted in the Canadian markets, as assets in sustainable retail mutual funds increased by 36% from the 2018 report, up to C$15.1 billion in the 2020 report.

Using environmental criteria in the evaluation process is one way investors can mitigate long-term climate risks that are difficult to analyze and quantify. This approach also actively tilts investors away from companies with business models that will be harmed by climate change, while pointing investors towards those that thrive.

Fossil Fuel Divestment

A simple option for investors who seek to reduce exposure to fossil fuels through divestment of these stocks such as thermal coal or unconventional oil and gas stocks due to the carbon intensity of these fuels. Divestment can also extend to utilities and energy producers. Broad divestment may represent a strong sector bet since the transition to low carbon energies has not yet been fully formed.

Investing in a Green Transition

Another approach is, to increase exposure to companies providing climate solutions by investing in renewable energy, energy storage, water, forestry or energy efficient products that capture upside opportunities in addition to mitigating risks. In the fixed income markets, allocations can be made into green or climate bonds although the number of options remain low. Another strategy is to consider an issuer’s climate strategy and evidence of a transition management plan. This analysis of a company’s preparedness to navigate climate transition compared to peers can differentiate companies beyond the scope of the energy and utilities sector, assessing management of other transition and physical risks.

Low Carbon

Investors may take a more nuanced look at climate risk and consider the potential role traditional energy and utility companies could play in the transition to a green economy by taking a more selective approach to reducing their exposures. Assessing portfolio level carbon emissions and exposure to future emissions as converted through fossil fuel reserves, allows an investor to minimize exposure to the heaviest issuer footprints while maintaining exposure to issuers that are in transition.

Stewardship

A growing cohort of investors are expressing their focus on climate risk through the stewardship process. Stewardship expectations on the low carbon transition can be articulated through activities in industry bodies, feedback to regulators and index providers and through more traditional mechanisms like voting proxies and conducting engagements.

The focus is now on the evolving nature of global regulatory regimes, and investors engaging actively in these conversations. A group of Canadian pension funds recently called on the U.S. Securities and Exchange Commission to leverage the TCFD framework to standardize mandatory reporting for listed issuers related to climate risk. Many collaborative engagement initiatives have demonstrated results that are encouraging. For example, Climate Action 100+ is an initiative representing 615 members, representing $55 trillion in combined assets under management. The goal of this initiative is to enhance corporate strategies to meet climate change goals and calls for the companies who are emitting the most carbon to achieve net zero greenhouse gas emissions by 2050 and to develop clear transition plans. The results are compelling and already six of the largest oil and gas companies and four of the largest mining companies in Europe, as well as some Australia and American peers have made the commitment to achieve net zero by 2050 or earlier.

Key Considerations

Implementing an effective decarbonization strategy can follow any number of approaches. For example, before investors choose to divest from an issuer, they should be aware that divestment prevents engagement. Constructive dialogue could enhance a company’s transition to low carbon business models. Layering in a carbon foot printing process to account for the whole spectrum of a portfolio’s carbon exposure or complementing the approach by targeted investment into companies that provide green products and services, such as renewable energies, could add an additional level of sophistication to a climate-aligned portfolio. A thoughtful approach to portfolio construction can leverage the spectrum of tools to meet investor objectives. The use of these tools can be revisited and adjusted over time to adapt to the climate transition and the decarbonization of the markets.

As momentum to address climate change in the financial markets builds through governmental commitments and monetary policy, the discussion around how to integrate climate change into the investment management process will be amplified in Canada. Canadian investment trends that adopt climate-aligned investment strategies is growing and is poised to continue. Plan sponsors can begin addressing this now by assessing whether the stewardship activities being conducted on their behalf are aligned with mitigating and managing climate risk and can consider which parts of their portfolio represent the biggest climate risks as a means of identifying a path forward.

IMPORTANT INFORMATION. For Use with Institutional Investors/Financial Professionals Only. Not For Retail Use. For Asia-Pacific markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Opinions and forecasts discussed are those of the author, do not necessarily reflect the views of Northern Trust and are subject to change without notice.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. Information is subject to change based on market or other conditions.

Forward-looking statements and assumptions are Northern Trust’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Past performance is no guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by Northern Trust. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For additional information on fees, please refer to Part 2a of the Form ADV or consult a Northern Trust representative.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.

[1] 2020 Canadian RI Trends Report, RiA

Julie Moret, Global Head of Sustainable Investing and Stewardship, Northern Trust Asset Management

Julie Moret is the global head of Sustainable Investing and Stewardship for Northern Trust Asset Management responsible for overseeing the firm’s sustainable investing and global engagement policies, foster research and product development agendas and advance portfolio integration across asset classes. She leads a diverse team of global ESG specialists skilled at applying the expertise and insights of NTAM to deliver highly efficient sustainable solutions as well as shepherding the stewardship team as they identify long-term risks that may pose challenges for shareholder value and engage with senior management of portfolio companies.

Julie began her 20-year career as a quantitative risk consultant at Barra before moving on to hold portfolio / investment risk strategy roles at Aviva Investors.

Prior to joining Northern Trust, Julie was global head of ESG at Franklin Templeton. During her tenure, Julie was responsible for establishing and leading the firm’s efforts to evolve the integration of ESG considerations into the investment process and risk framework, as well as shaping product development globally. In addition she served on a number of industry bodies to further the adoption of ESG integration best practice, such as the Investors Advisory Group at SASB-Sustainable Accounting Standards Board and the Sustainable and Responsible Investing committee at the IA- Investment Association and ICI’s ESG working group

Emily Lawrence, North American Director of Sustainable Investing Client Engagement, Northern Trust Asset Management

Emily Lawrence is North American Director of Sustainable Investing Client Engagement at Northern Trust Asset Management where she is responsible for client engagement and partnership regarding Northern Trusts’ sustainable investing capabilities. Emily has 14 years’ experience collaborating with clients to support the development of actionable approaches to sustainable investing. In addition to representing the investment platform, Emily collaborates directly with clients to conduct trainings and facilitate discussions on concepts, themes and trends through individual meetings, webinars and thought leadership.

Prior to joining Northern Trust, Emily managed research production for MSCI ESG Research’s Screening Research and Bespoke Research teams. She is also an active member of the Northern Trust Sustainable Investing Council, Proxy Voting Committee and Executive CSR Council. An advocate for diversity, equity and inclusion in the investment management industry, Emily has served as a mentor for young professionals through the Women in ETFs mentorship program starting in 2017 and has co-chaired the Events Committee for the Diversity Project North America since 2019. She sits on the ESG sub-committees for a variety of industry bodies including DCIIA, ICI, and ABA. Previously, Emily was appointed to the Principles for Responsible Investment working group focused on Active Ownership and the Sustainable Development Goals and the Climate Action and Resiliency Plan Working Group for the government of Evanston, IL.