Articles of Interest

A Second Chance for Defined Benefit Plans?

We live in a time where interest in retirement plans is in decline. We could even say that total rewards is becoming less "total," focusing more on base salary and bonuses. Given the recent years of high inflation and the soaring cost of housing, it's understandable that people would prioritize higher wages to cover living expenses and achieve homeownership rather than saving for retirement. Even though some young people receive help from their parents for a down payment on a first home, most are not so fortunate. The steep rise in costs for basic needs like housing and food is a significant burden, preventing people from saving adequately for retirement or, worse, forcing them to postpone the moment they will begin saving to fund properly their retirement.

With a life expectancy that has greatly improved, future retirees of this generation will need substantial savings to enjoy a long and comfortable retirement. Capital accumulation plans, which allow to save a significant amount for retirement if used properly, are today’s preferred type of retirement plan in the market, while defined benefit plans are fading away.

The decline of defined benefit plans began in the second half of the 1990s, when many employee groups believed they could achieve better investment returns than those generated by investment professionals. Employees then began requesting that their employers change their defined benefit plans for capital accumulation plans. The 2000s brought a wave of plan restructuring measures or closure of retirement plans, as both public and private employers were faced with massive actuarial deficits following various financial crises and an important increase in life expectancy.

Capital accumulation plans can allow for substantial savings, but there’s no guarantee that these savings will be sufficient for a secure retirement. As we approach 2025, are we ready to reconsider defined benefit plans for new generations of workers to avoid intergenerational inequity and ensure that they can live a retirement without the risk of running out of money?

Are Government Retirement Benefits Programs Sufficient?

Government efforts to enhance the pension benefits from the Canada Pension Plan and Quebec Pension Plan have increased the retirement benefit from 25% to 33.33% of eligible earnings (up to the maximum called maximum pensionable earnings). Additionally, this earnings limit has been raised by 14%, further increasing the pension paid by government retirement benefits programs. The federal government has also taken steps to boost the Old Age Security pension by 10% for people aged 75 and older, as a form of longevity benefit.

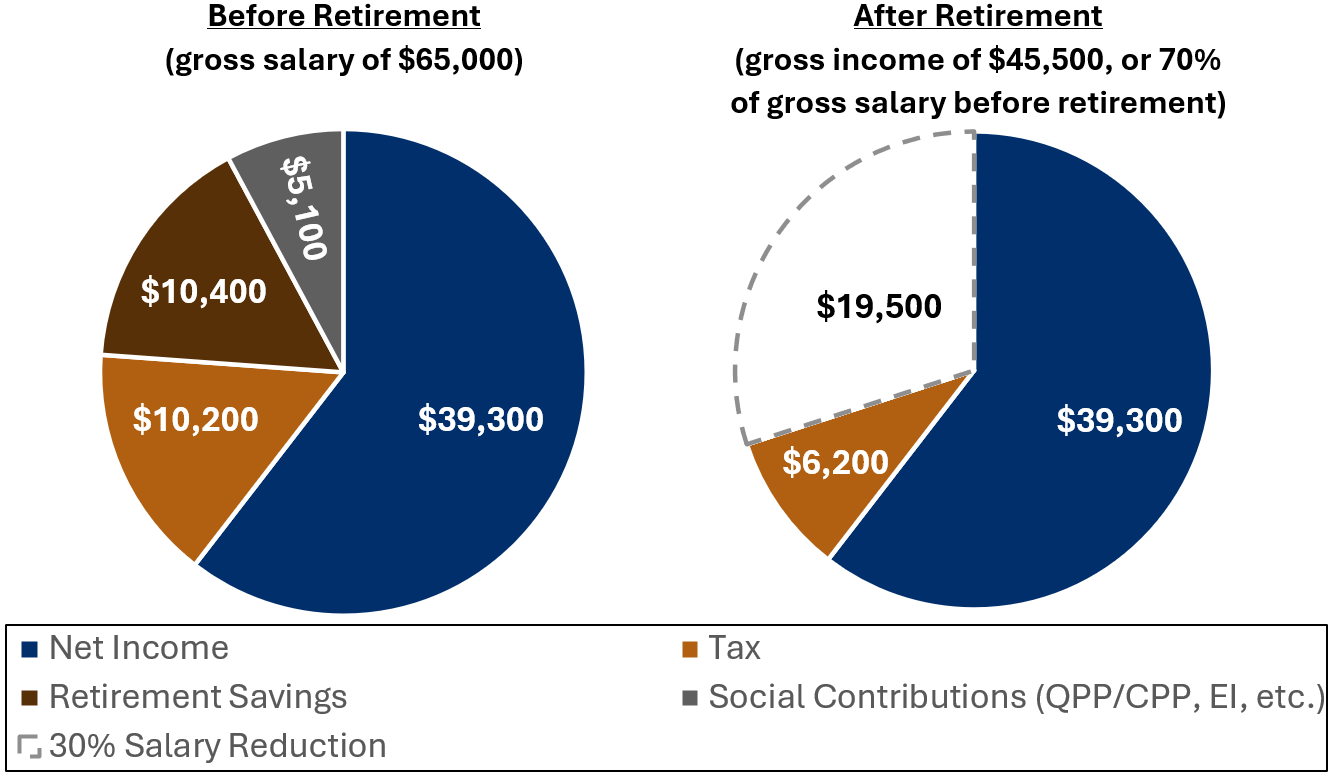

Despite these enhancements to government retirement benefits programs, these measures remain insufficient to provide most people with an adequate retirement income. The income from government retirement benefits programs would cover only about half of the net paycheck for an employee earning between $50,000 and $75,000 per year. Can someone live a comfortable and proper retirement if their income becomes half of what it was pre-retirement? Many would say no.

How Much Do I Need to Live a Comfortable Retirement?

The existential question "How much savings does a person need for retirement?" persists over time. Government retirement benefits programs provide a basic retirement income that should be supplemented by employees' savings. Aiming for a 100% income replacement isn't necessary. The answer to the income replacement question varies from person to person, but it’s often close to the famous rule of 70% of pre-retirement gross income. The 30% income reduction accounts for certain expenses, social charges, and retirement savings that are no longer required after retirement, as well as lower taxes due to lower income brackets.

Without targeting 70% precisely, we can easily assume that someone aiming to replace between 60% and 80% of their pre-retirement income could maintain a similar lifestyle during retirement. If we assume that government retirement benefits programs replace about half of pre-retirement income, there remains a gap of between 10% and 30% of income to achieve a financially comfortable retirement.

Is Offering a "Reasonable" Defined Benefit Plan Possible?

Currently, capital accumulation plans are the most popular in the market. Simple to understand, they carry no risk of financial deficits, which is not the case with defined benefit plans. However, they require more employee education on retirement planning, covering savings, investing, and, ultimately, decumulation. Decumulation is the most complex part, leaving employees to decide how fast to withdraw their funds or whether to purchase a life annuity from an insurer (the less popular option when interest rates are low). Many tools have been developed over time to address these needs, but much work remains in educating employees on the importance of participating in these plans to gain the maximum benefits and understand the impact of management fees, that can be very high at times.

When it comes to a defined benefit plan, concerns are often around deficit risks and the annual costs of pension accrued by employees. Yet, is it still possible nowadays to offer a “reasonable” defined benefit plan? Such a plan should be straightforward, aligned with government retirement benefits programs eligibility age, and based on employees’ salaries. The benefits that would best meet these objectives are the following:

- Retirement age at 65, like government retirement benefits programs;

- Career-average plan of 1% of earned income;

- Ad hoc indexing in the event of significant surpluses.

By keeping benefits reasonable and avoiding incentives for employees to retire before age 65, a "reasonable" defined benefit plan is feasible. The ultimate goal is to help employees cover between 10% to 30% of the income gap that will supplement government retirement benefits programs.

This “reasonable” defined benefit plan may seem costly based on the history of closed defined benefit plans. However, with a contribution of just 5% of salary from the employer and the same from the employee, such a plan could be viable. This retirement plan, accruing a pension at 1% of an employee’s annual income, could guarantee a retirement income covering 20% to 25% of pre-retirement income, closing the gap with government retirement benefits programs to achieve a total of 70% income replacement goal.

Could Defined Benefit Plans Make a Return?

Defined benefit plans' history may not do them justice, yet they have served a hard-working generation that now enjoys a comfortable retirement. Today, almost only public sector employees benefit from a defined benefit plan. However, today’s tools to build, fund, and manage defined benefit pension plans have evolved and are now better suited to counter economic fluctuations.

The kind of retirement employees want lies in the hands of the younger generation, who must decide whether securing their financial future is worth prioritizing today or whether they will postpone this issue, risking much less generous retirement benefits. Both employers and employees should invest in funding retirement plans, whatever the type of retirement plan. To support employees during this pivotal stage of their life, defined benefit plans are the only one providing a guaranteed fixed income for life. Today’s funding mechanisms can help prevent actuarial deficits, making these plans more appealing than ever. With this perspective, perhaps defined benefit plans will be given a second chance.

Jean-Sébastien Côté, FSA, FCIA, Senior Consultant at Optimum Actuarial Consulting.

Jean-Sébastien Côté is an actuary specializing in pension plans, with over ten years of experience in the funding and administration of accumulation pension plans and defined benefit plans. He leverages his expertise to help employers and plan sponsors navigate the financial and regulatory challenges associated with pension plan management, while providing tailored strategies to ensure the financial security of participants. In addition to his professional responsibilities, Jean-Sébastien actively contributes to thought leadership and innovation in the pension sector through his numerous publications.

Linkedin : www.linkedin.com/in/js-cote-oac