Articles of Interest

IG Private Fixed Income And Solutions To LDI Conundrums

For pension plan sponsors, a liability-driven investment (LDI) approach can often involve a number of tradeoffs. How can plans invest in order for their assets to have strong correlation to corporate-linked liabilities, while still providing sufficient diversification to minimize the impact of downgrades and defaults? How much return potential should plans sacrifice to better hedge liabilities? In this piece we discuss these challenges and how an asset class like investment grade (IG) private fixed income can help.

Correlation versus diversification?

One of the most paradoxical demands of an LDI program is its dual goals. The first is its goal of hedging liabilities, measured on a discount curve based on a narrow subset of corporate and provincial bonds. The second goal is ensuring that the portfolio contains sufficient diversification to avoid overconcentration across issuers or sectors that could negatively impact the portfolio through downgrades and defaults.

The need to answer this correlation versus diversification question has become more pressing for plan sponsors, as they have moved down their glidepaths and allocated more to fixed income assets. The goal of many multi-asset LDI solutions is to find the right mix of assets such that the benefits of a more diversified portfolio outweigh any adverse impact on the overall hedging strategy.

The introduction of a diversifying asset class often introduces additional tracking error versus the liabilities. For example, when plan sponsors use non-investment grade issues that fall outside the discount rate methodology used for most purposes, they are introducing an asset class into their portfolio that is not directly used in valuing their liabilities. However, because of the correlation to more highly rated bonds and the added diversification benefits, the potential upside of expanding the investible universe outweighs the downsides of introducing a slightly less-correlated asset for most plan sponsors. While this example is very straightforward, most other asset classes outside of public fixed income markets introduce a degree of tracking error relative to the liabilities that must be weighed relative to the benefits of a more diversified portfolio.

Hedging versus outperforming the liability

Plan sponsors face another tradeoff when thinking about balancing the risk and return goals of an LDI program. As plan sponsors look to lock in their funded status gains, they typically allocate away from growth assets such as equities to liability-hedging assets such as corporate and provincial bonds. This helps reduce the funded status volatility but also sacrifices some of the upside from the growth allocation.

Many plan sponsors are comfortable with this tradeoff – as they move down their glidepaths, the value of protecting their funded status outweighs the potential upside that comes from taking more risk. Other plan sponsors choose to achieve their hedging goals synthetically, utilizing leverage or swaps to add duration while maintaining their growth allocations. However, these sponsors then face challenges in hedging the credit exposure inherent in their liabilities.

In general, the more we work to make the assets look and behave like the liabilities, the less potential upside we have to keep pace with some of the “unhedgeable” components inherent in pension plans. Such components include the fact that the discount curves used to value liabilities are immune to possible defaults and downgrades, and that liabilities themselves are impacted by factors such as increased longevity.

Does IG private fixed income “thread the needle?”

IG private fixed income might be positioned right in the middle of these tradeoffs. The asset class encompasses loans and debt securities issued by companies or entities outside of public capital markets. Issuance is primarily fixed rate, IG debt instruments, with tenors from 5–30 years but with structural protections that surpass those typical for public bonds, including collateral and maintenance covenants. As IG private fixed income transactions are generally more customized and less liquid than public bonds, investors are paid a spread premium over comparable public bonds.

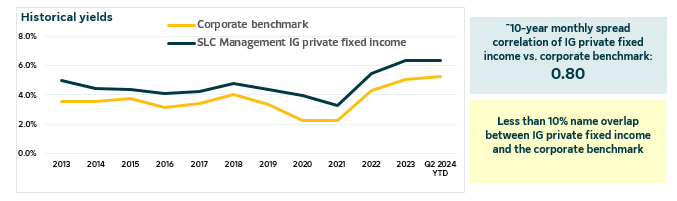

Correlation with diversification

IG private fixed income can be well positioned to provide both the potential benefits of correlation and diversification for plan sponsors. Firstly, and critically for LDI investors, IG private fixed income issues are typically priced relative to the interest rates and spreads underlying traditional IG public bonds. This gives them a direct connection to the discount curves used to value plan liabilities. This correlation makes the asset class a natural fit for a portfolio attempting to hedge liabilities on a solvency or accounting basis.

Secondly, investing in IG private fixed income provides plans with access to a range of IG issuers and sectors outside public markets. Examples include major professional sports leagues, large accounting firms and asset managers. This breadth of opportunities can be critical for plan sponsors looking to reduce their concentration risk to names in the public markets.

The following exhibit illustrates this balance of correlation and name diversification, utilizing SLC Management’s combined IG private fixed income pool1 as a proxy for IG private fixed income:

Sources: Bloomberg, SLC Management, 2024. Data include U.S. currency and fixed rate transactions. Data for IG private fixed income represent the weighted average of SLC Management’s combined investment grade private fixed income pool.1 Data for the corporate benchmark represents the weighted average benchmark of investment grade public bonds that are equivalent in rating, maturity and sector. Past performance is not indicative of future results. The ~10-year monthly spread correlation was determined using data from Bloomberg and StoneCastle.

A hedging asset that outyields the liability

Similarly, IG private fixed income can allow plan sponsors to both closely hedge pension liabilities and add excess return to keep pace with some of the previously referenced unhedgeable components of pension plans.

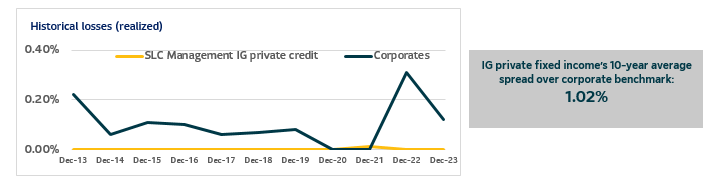

As illustrated previously, IG private fixed income maintains a close correlation to pension discount curves. However, the asset class may also provide additional compensation in return for investing outside public markets. This yield premium typically ranges from 30–300 basis points depending on the nature and complexity of the deal. Unlike public markets, where higher yields are typically seen as compensation for taking additional credit risk, investors in IG private fixed income are instead being compensated for the lower liquidity of the asset class and the additional complexity involved in sourcing, underwriting and maintaining these private deals. This additional yield and lower loss experience can be critical for plan sponsors as they look to keep pace with downgrade-immune liability discount curves.

The following chart illustrates the lower default and loss experience of IG private fixed income relative to IG public markets alongside historical spread premiums. The yield premiums and maintenance covenants associated with IG private fixed income result in these attractive risk–return characteristics.

Sources: Bloomberg, SLC Management, Moody’s, 2024. Shown for illustrative purposes only. Data for IG private fixed income represent the weighted average of SLC Management’s combined investment grade private fixed income pool.1 Data for the corporate benchmark represents the weighted average benchmark of investment grade public bonds that are equivalent in rating, maturity and sector. Past performance is not indicative of future results.

Many pension plans are in a favorable position when it comes to managing liquidity. Heavy allocations to fixed income assets typically generate more than enough income to meet benefit payments. Meanwhile, major liquidity events such as pension risk transfer activities normally have a significant lead time providing plan sponsors a sufficient window to liquidate assets. It is also worth noting that IG private fixed income can provide some liquidity through fund vehicles. Such solutions often have enhanced liquidity characteristics compared to the IG private fixed income market overall, and do not have the lock-up periods associated with non-IG private fixed income.

An old solution for a new challenge

IG private fixed income has been around for decades as a hedging asset. However, the largest life insurers have traditionally monopolized the space, utilizing their scale and depth of expertise to originate transactions. This has been a large driver of the annuity buyout market, as life insurers are able to price transactions under the assumption that they will benefit from the attractive yields and downside protection available in IG private fixed income.

Barriers to entry in this market have historically ruled out many participants, as the private and specialized nature of the asset class meant investors needed a deep bench of credit analysts, underwriters and originators to build the necessary relationships with issuers and other market participants. However, more recently we have seen vehicles specifically designed to provide improved liquidity, market pricing and access for plan sponsors. This makes IG private fixed income now available more broadly to both large and smaller plan sponsors looking to use these solutions in the LDI program.

While no asset class provides a silver bullet for plan sponsors facing tradeoffs in their LDI program, we believe IG private fixed income might be well positioned to help address those tradeoffs.

1. SLC Management’s IG private fixed income pool comprises all U.S.-dollar investment grade private fixed income commitments made by SLC Management for use by all clients, including Sun Life Financial’s general account, other insurance pension and separate account clients and SLC Management’s private fixed income funds.

Disclosures

© 2024, SLC Management

Investment-grade credit ratings of our private placements portfolio assets are based on a proprietary, internal credit rating methodology that was developed using both externally-purchased and internally developed models. This methodology is reviewed regularly. More details can be shared upon request. There is no guarantee that the same rating(s) would be assigned to portfolio asset(s) if they were independently rated by a major credit ratings organization.

Yield is a moment-in-time statistical metric for fixed income securities that helps investors determine the

value of a security, portfolio or composite. Yield strictly measures a bond or portfolio's cash flows and has no bearing on performance.

SLC Management is the brand name for the institutional asset management business of Sun Life Financial Inc. (“Sun Life”) under which Sun Life Capital Management (U.S.) LLC in the United States, and Sun Life Capital Management (Canada) Inc. in Canada operate. Sun Life Capital Management (Canada) Inc. is a Canadian registered portfolio manager, investment fund manager, exempt market dealer and in Ontario, a commodity trading manager. Sun Life Capital Management (U.S.) LLC is registered with the U.S. Securities and Exchange Commission as an investment adviser and is also a Commodity Trading Advisor and Commodity Pool Operator registered with the Commodity Futures Trading Commission under the Commodity Exchange Act and Members of the National Futures Association.

Unless otherwise stated, all figures and estimates provided have been sourced internally and are as of June 30, 2024. Unless otherwise noted, all references to “$” are in U.S. dollars. Past performance is not indicative of future results.

Nothing herein constitutes an offer to sell or the solicitation of an offer to buy securities. The information in these materials is provided solely as reference material with respect to the Firm, its people and advisory services business, as an asset management company.

Market data and information included herein is based on various published and unpublished sources considered to be reliable but has not been independently verified and there is no guarantee of its accuracy or completeness.

This content may present materials or statements which reflect expectations or forecasts of future events. Such forward-looking statements are speculative in nature and may be subject to risks, uncertainties and assumptions and actual results which could differ significantly from the statements. As such, do not place undue reliance upon such forward-looking statements. All opinions and commentary are subject to change without notice and are provided in good faith without legal responsibility. Unless otherwise stated, all figures and estimates provided have been sourced internally and are current as at the date of the paper unless separately stated. All data is subject to change.

This information is not intended to provide specific financial, tax, investment, insurance, legal or accounting advice and should not be relied upon and does not constitute a specific offer to buy and/or sell securities, insurance or investment services. Investors should consult with their professional advisors before acting upon any information contained in this paper. An investor may not invest directly in an index.

No part of this material may, without SLC Management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

This material is intended for institutional investors only. It is not for retail use or distribution to individual investors. Nothing in this presentation should (i) be construed to cause any of the operations under SLC Management to be an investment advice fiduciary under the U.S. Employee Retirement Income Security Act of 1974, as amended, the U.S. Internal Revenue Code of 1986, as amended, or similar law, (ii) be considered individualized investment advice to plan assets based on the particular needs of a plan or (iii) serve as a primary basis for investment decisions with respect to plan assets.

Ashwin Gopwani, Managing Director, Head of Retirement Solutions, SLC Management

Ashwin leads the retirement solutions team efforts across both Canada and the U.S. helping to deliver the full SLC Management platform to our clients and prospects.

Ashwin and his team are responsible for developing innovative customized investment portfolios, leading analytics and management reporting for clients and contributing to the development of market insights that can help companies manage the risks in their portfolios.

Ashwin joined Sun Life in 2017 after 10 years of experience at a leading Canadian consulting firm where he consulted on valuations, asset liability studies and plan design for a variety of pension plans, foundations and endowment funds.

Ashwin holds a Bachelor of Mathematics degree from the University of Waterloo and is a qualified actuary, a CFA charterholder and a CAIA charterholder.