Articles of Interest

Is Occam’s Razor Shaving Your Investment Returns?

Occam's razor is the problem-solving maxim that when considering two competing ideas to explain a phenomenon, the simpler one is usually right. Complexity has only increased in recent decades in the financial markets as traditional 60/40 mixes of public-market equities and bonds have been set aside in favour of allocations to hedge funds, private credit, private equity, real estate and so on. Has this complexity paid off? Is Occam’s razor wrong?

Bias for action

When crisis strikes, stakeholders often default to the conclusion that “we cannot just hold the line; we have to do something.” When we spoke with our clients in the midst of the great financial crisis, they were understandably concerned about their portfolios and many wanted to know what we were doing. The fact was they had high quality, liquid holdings and when considering that the tentacles of risk could appear in surprising places through the banking system, the prudent course was not to add complexity to the situation by launching a series of trades, but to hold the line. This somehow seemed wrong at the time but proved correct.

As money managers (and fellow humans) we are not immune to feeling this impulse to act, but when you have done a good job in advance of understanding risk, assessing quality, and diversifying holdings, the panic-now think-later mantra can be incredibly value destroying.

The same bias for action can appear in investment trustee meetings when a money manager’s recent performance pulls longer-term numbers below benchmark. There may be an impulse to make a change but more often than not, the prudent course of action is understanding the drivers of recent underperformance and staying the course.

Value investors saw this patience pay off when interest rates spiked in 2022 and markets realized that a big driver of 10+ years of great equity performances had been more about discounting cash flows than necessarily manager skill. That included “growth stocks” in general (which are harder hit by rate increases), real estate investment, and arguably low volatility strategies, whose smart engineering ended up creating equity funds that were effectively bond proxies – and so hit the wall when rates rose.

This patience is especially important when your investment manager is protecting you from getting burned by the current fad. Many managers, us included, faced tough questions through the dot-com craze as equity performances fell double-digits behind benchmarks, but reaped enormous rewards as those same darlings crashed.

Today discipline is required as billions are poured into AI stocks – companies that will play an important role in many industries but, in our view, carrying valuations far in excess of what profitability could plausibly be achieved in the foreseeable future.

Impatience is not rewarded

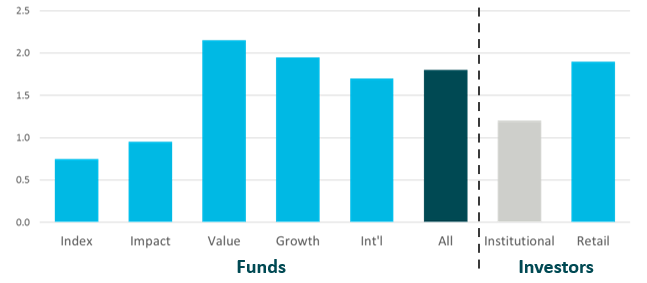

The bias for action can show up as “performance chasing” in the mutual fund universe as well. Unfortunately, there is ample evidence that hopping between mutual funds, rather than buying and holding, has cost investors dearly. Figure 1 illustrates the findings of a George Mason University study that quantified the “return gap” that emerged from the practice over 10 years. Regardless of strategy type, region, or even investor type, investors lost on average between 1-2% per year by selling last year’s “loser” and buying the hottest current performance. In other words, the worst off would be >20% poorer after a decade versus if they’d just set it and forget it.

Figure 1: The annualized, 10-year return gap for mutual fund investors, by type (lost performance per year in percentage points)

Source: Derek Horstmeyer, George Mason University.

Researchers Goyal and Wahal found similar results for institutional investors who had replaced a manager primarily based on performance. They looked at 412 transitions between 1996-2003 and found that on average the new managers – despite outperforming coming in – underperformed the ones they replaced by 0.8% over the subsequent three years.

The allure of complexity

Back to our theme of Occam’s Razor, another bias that can influence investor behaviour is the irrational over-valuing of complex solutions over simple ones. The risks to a less sophisticated investment committee are plain: complicated investment structures and products cannot be assessed without comprehension and the ability to monitor and track risk. This risk does not lay solely at the feet of institutional clients, however: one needs only recall the blind faith by so-called sophisticated investment professionals in the AAA quality of sub-prime collateralized debt obligations (CDOs) in the mid-late 2000s. A lack of visibility into what made CDOs tick (and a lack of due diligence by their backers and buyers) created unique risk that couldn’t be effectively managed and ultimately brought the financial markets to the brink of ruin.

We should be clear: not all complexity is bad, and certainly not all is toxic. If plans do push into less traditional assets classes, they need to do it in a way that matches their governance capabilities. In short, do you have sufficient experience on your investment committee with the strategies being considered? Do you have professional help (consultants, investment managers) who understand your organization, the strategies being considered, and can communicate clearly to you the risks and opportunities inherent in them?

In this article, former consultant and author Mark Higgins maps the life cycle of new ideas in financial markets. He describes them as Formation (a legitimate need arises which is solved by a new product or approach); Early Phase (early entrants capitalize and make outsized returns in the new product or approach); and Flood Phase (a barrage of products are created and sold, sold, sold down the line). His sniper rifle is pointed at alternative assets, specifically the large “flows” into private credit in recent years, which indicate to him that we’re knee-deep in floodwaters at present but don’t perhaps realize it.

In our view, the risk is that while private assets may still be valid and valuable in certain circumstances, the original triggers to go down this road in the first place are largely gone. Specifically, private assets helped solve tough solvency tests (now softened), made so by low rates (now higher), and a desire to dampen market volatility (now less important). Given the changed conditions, are investors solving yesterday's problem with products with high fees, severe legal complexity, limited liquidity and visibility, and that hamper portfolio rebalancing – when public bond yields and the equity market premium can get you there with none of that?

Complexity in the cross hairs

Even the most capable and well-resourced professional groups in our industry can face challenges at times. In May 2024 a Globe and Mail article criticized the Canada Pension Plan (CPP) for failing to beat an index portfolio over the 18 years since it had switched from a simple, passive approach to pursuing a complex, active management strategy. Throwing rocks is easy but like a good investment, this criticism would benefit from a little vetting.

In the most-current year the market had been roaring, with its benchmark delivering 19.9%. CPP’s 8% was modest by comparison, but that is part of its design. Simple end-point returns ignore the risk of the portfolio, the future expectations of the portfolio, and the portfolio’s ability to protect capital in down years – an especially important feature for a national pension plan. If one simply dialed back one year, the CPP fund was ahead of what a simple index strategy would have delivered, by $47 billion!

Measurement complexity and Goodhart’s Law

In investing there is a fallacy that having more data necessarily contributes to better decisions. Consider how much time you spend clearing your inbox – does it always make you more efficient and effective? Maybe not!

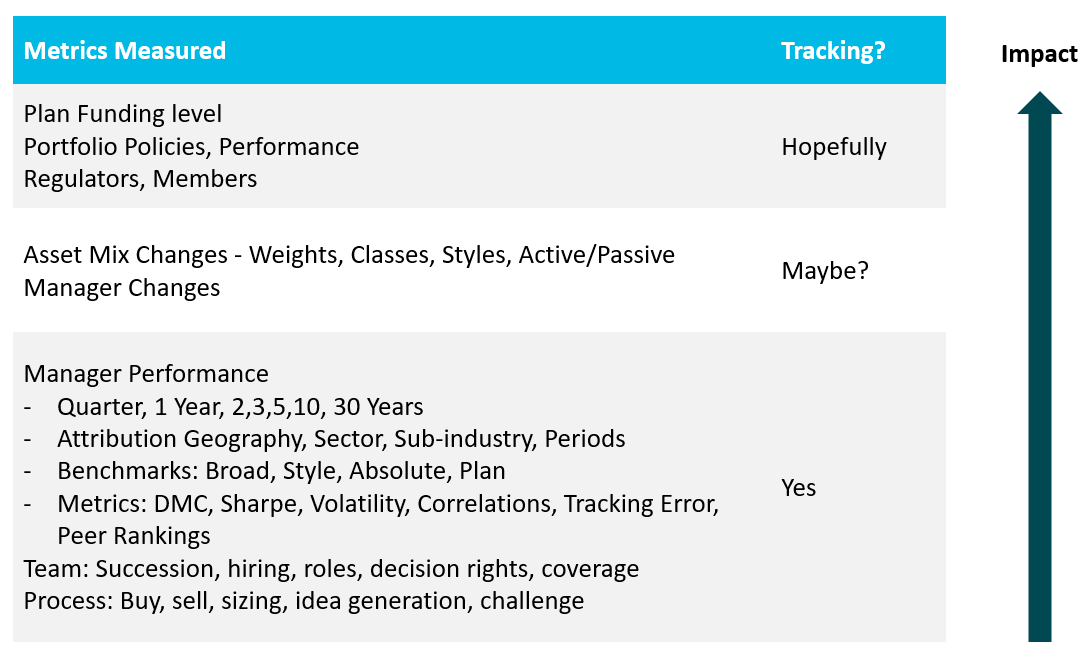

The same fallacy can crop up when measuring investment performance. A plan sponsor or consultant may generate multiple, detailed measures of quarterly portfolio performance by each manager but lose sight of how all of those portfolios aggregate up. In our experience, there are three buckets of impact and the punchline is: the more finely you measure, the less likely those measurements will impact the fund’s success long term. See Figure 2.

As Goyal and Wahal found, tracking manager changes (middle section) is an important opportunity for learning whether decisions were taken effectively. The same is true of changes in benchmark and asset mix, especially when new strategies are funded out of old ones. Did it lower risk as you thought? Did it augment performance as you hoped? Was the illiquidity as good or bad as you thought? These kinds of decisions are often not really being formally tracked, and yet can have a huge impact on portfolio outcomes.

Figure 2: The inverse relationship between measurement detail and impact

Source: Leith Wheeler Investment Counsel.

Goodhart’s Law describes this phenomenon taken to its extreme, where the measure becomes the goal. Imagine a large fund with multiple, siloed groups (real estate, public equities, private equity, and so on), and each group is tasked with a specific goal. The groups then target their own goals, assess risk, establish asset mix, choose style(s), and benchmark managers. The overall fund has specific goals – the most important ones – but without oversight the amalgamation of all the sub-groups may not achieve them. The individual measures become the goal. Total Portfolio Management is a solution some funds have adopted, which can better connect the portfolios to the top-level goals, utilizing mix but also factor drivers and a dynamic allocation process.

Investors need not eschew all innovative ideas that add complexity to their lives, but sometimes, when an idea sounds smart because it seems hard to understand… consider what Occam’s Razor would suggest.

Marc is a Principal and Portfolio Manager - Institutional Clients with Leith Wheeler Investment Counsel. He joined the firm in October 2015 after more than 20 years in the pension and institutional investment industry. His career includes roles as an Actuary and Investment Consultant at a large multi-national consulting organization and as a Senior Investment Analyst at an alternative asset management firm. Marc’s past clientele have included corporate, government, and union pension plans, as well as endowment funds and First Nations trust funds. Marc is a Chartered Financial Analyst (CFA®) charterholder and a Fellow of both the Canadian and UK Institutes of Actuaries.

Mike is a Principal and Vice President, Marketing & Communications at Leith Wheeler Investment Counsel. He joined the firm in 2017, bringing with him both investment industry experience as an investment banker, equity analyst, and institutional portfolio manager, and as a broadcast journalist with the CBC. Mike holds Finance and Master of Journalism degrees from the University of British Columbia and is a Chartered Financial Analyst (CFA®) charterholder and Past President of CFA Society Vancouver (2021). He also hosts CFA Institute's flagship global investment podcast, Enterprising Investor, where he interviews leading minds from around the world on current issues and opportunities in our industry.