Articles of Interest

Protecting Canada’s Pension System Post-Pandemic

A study released by the Canadian Centre for Economic Analysis on the economic impacts of Canadian public sector pension plans (CPSPPs) found that every $10 of pension paid to a retired member generates $16.72 in economic activity. In total, CPSPP activities support over $82 billion in GDP and generate $21.4 billion in tax revenue each year, which would cover the entire annual budget of Manitoba’s government.

The study demonstrates that Canada’s public sector pension system is a unique asset that benefits pensioners and broader communities of Canadians across the country. It provides widespread and intergenerational economic value to Canada by channeling reliable, taxable spending into rural and urban communities, and secures the healthy deferred tax base that the country needs. The findings substantiate over a decade of research on the superior efficiency and value of the Canadian defined benefit (DB) pension design model (the “Maple Model”) – that it is a sustainable pension model that should be protected and expanded to more workplaces.

Economic Contribution: Total Tax Revenue per $10 of Pension Payment

The Maple Model is considered one of the best pension investment models in the world[1]. Its international reputation and domestic success stem from its unique combination of sophisticated investment expertise, strategic use of alternative investments, independent governance structure and prudent risk management. Several public sector plans in the country follow it today, including the Maple Eight[2], which collectively manage more than $1.6 trillion in assets. Along with smaller Canadian pension plans that follow the same model, they drive one of the strongest retirement systems in the world and contribute significantly to national prosperity.

With a successful, homegrown invention that has been pressure-tested through various economic storms and proven to deliver retirement security to 5.26 million active and retired members, Canadian plan sponsors possess a design framework that can be adapted to expand attractive pensions to private sector workplaces. Many of these workplaces currently have no retirement savings program in place at all. High quality, expertly managed pensions remain essentially exclusive to public sector workers, as the pension coverage gap and retirement insecurity in Canada continue to grow.

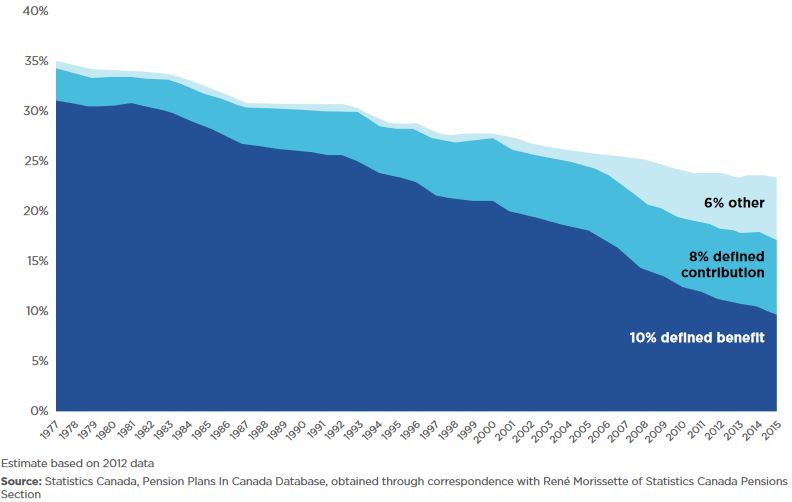

In 2005, there were 2.65 million active members of CPSPPs, growing to 3.41 million active members as of 2019. During the same period, membership of private sector pension plans stagnated, with 3.015 million active members in 2005, rising slightly to 3.020 million in 2019. The recent paper The Value of a Good Pension illustrates the decline in private sector workers with DB pension arrangements, which in 2015 dipped to one-third of 1970s levels. Today, almost two-thirds of Canadians have no workplace pension at all, and less than 10 per cent of private sector workers have a DB pension.

Proportion of Canada’s Private Sector Workers Participating in an RPP, 1977-2015

The diminishing supply of DB pensions in the private sector due to perceived high costs and high risk of pension administration could potentially put all pension plans at risk. The best way to mitigate this risk and better secure existing DB plans is by expanding coverage in the private and not-for-profit sectors. Extending DB coverage beyond the public sector will help engrain DB pensions as one of the most effective retirement savings vehicles available and strengthen the Canadian pension system. Plan sponsors should look to the structural blueprint in the Maple Model design to welcome more workers into Canada’s world-class pension system.

Adapting the Maple Model to the Private Sector

The Maple Model design harmonizes key investment and efficiency principles into a single, well-managed fund. Pooling contributions from multiple employers allows plans to leverage economies of scale and lower the average costs. The large size grants the plans access to a wide range of asset classes, such as private equity, real estate and infrastructure, and the ability to employ complex investment strategies to generate added value for members. Using an independent governance structure, the model maintains a focus on long-term sustainability and risk management under the direction of highly specialized pension and investment experts, a lauded advantage of Canadian funds.

The size of the CPSPPs is one of the factors that provides greater stability and value for members by reducing operating costs. The ratio of assets under management to active members across CPSPPs is currently just over $350,000. This is twice that of the private sector plans at around $175,000 and maintains lower costs per member. Opening a large-scale, independently governed pooled plan helps to ensure that pensions will be paid to members even if the employer ceases to exist, a traditional weak point in single-employer DB plans that have resulted in underfunded plan wind-ups and heightened perceived risk of DB plans.

The Maple Model is most effective when plan maturity is low. Lower plan maturity provides a better cash flow profile for taking investment risk and reduces risk of intergenerational transfers of equity if managed appropriately. While the ratio of active members to retired members is not a complete measure of plan maturity, the CPSPP’s current ratio of 1.84 could be improved. Applying the Maple Model to the private sector, especially in higher growth industries, would further demonstrate its strengths and bolster the Canadian pension system.

One way to adapt and test collective plans in the private sector that borrow from the Maple Model approach would be to introduce a pension plan that is intrinsically accommodating to member growth and responsive to employee needs. Similar to CPSPPs that serve specific industries and employer groups in the public sector, such as healthcare, education and municipal services, private sector multi-employer plans that are industry or association-based could provide a foundational level of predictability in pension administration and management. It would also ensure workforce applicability, allowing the independent plan providers to strengthen its value proposition and meet the needs of its target employee classes and employers, which are becoming increasingly complex in the post-pandemic world.

Closing the Pension Coverage Gap

As the world recovers from pandemic-driven volatility and low interest rates, the case to expand Maple Model pensions is stronger than ever. The drastic pressure on the economy and financial markets pressure-tested the value of the Maple Model’s pension promise: DB members were able to confidently spend their monthly retirement benefits in their local communities in a predictable, stable way and pay taxes. As provincial governments look for ways to sustain small businesses, pensioner spending is part of the solution: 72% of the businesses supported by pensioner spending employ less than 10 people.

Today, employees are challenging employers to renew their commitment to employee financial wellness and retirement security. A survey of Canadian workers found that 77% believe employers have a responsibility to offer a pension plan so that employees can have adequate retirement income. Almost 85% say that all workers should have access to affordable and efficient retirement savings arrangements, both of which are characteristics of the Maple Model design. The demand is clear: workers want pensions and the peace of mind that they provide.

With the latest research and proven real-world resilience of DB pensions, the pension industry can better articulate and quantify the value of pensions to the Canadian economy and lives of working Canadians during economic highs and lows. However, to truly protect the pension system in the long term, innovations are needed to adapt and expand the Maple Model design, close the pension coverage gap in Canada, and establish pensions as a viable business, economic and societal solution.

Pensions in the post-pandemic world represent more than a simple retirement savings program. This is an opportunity to protect and promote Canada’s pension system for the enhanced value it brings to businesses, such as mitigating risk exposure and improving recruitment and retention in a dynamic talent pool. At the national level, pensioner spending is a robust engine of consumer spending that can drive economic growth and smooth over deferred tax revenue into the next generation. Helping workers in the private sector save towards lifetime retirement income is good for employees, employers, the economy and Canadians overall. For innovative and enterprising plan providers, the Maple Model design could be the key to unlocking retirement security for all workers and economic prosperity for generations to come.

Notes:

[1] Based on a comparative study between the Canadian model, Dutch model, UK Public Funds model, US Corporate Funds model and the US Public Funds model, which found that the Canadian model outperformed their peers in terms of investment performance and insurance against liability risks from 2004 to 2018. The Canadian model of public pension investment has been adopted by large pension and sovereign wealth funds in other jurisdictions.

[2] Canada’s eight leading pension plan investment managers, including AIMCo (Albert Investment Management Corporation), BCI (British Columbia Investment Management Corporation), CDPQ (Caisse de dépôt et placement du Québec), CPP Investments, HOOPP (Healthcare of Ontario Pension Plan), OMERS (Ontario Municipal Employees Retirement System), Ontario Teachers' Pension Plan, and Public Sector Pension Investment Board.

Sources:

Ambachtsheer, K., Nicin, M., “Improving Canada’s Retirement Income System: A Discussion Paper on Setting Priorities” (2020). Link

Bédard-Pagé, G., Demers, A., Tuer, E., Tremblay, M., “Large Canadian Public Pension Funds: A Financial System Perspective” (2016). Link

Canadian Centre for Economic Analysis, “The Economic Benefits of Canadian Public Sector Pension Plans” (2021). Link

Global Risk Institute, “The Canadian Pension Fund Model: A Quantitative Portrait” (2020). Link

Healthcare of Ontario Pension Plan, “The Value of a Good Pension: How to Improve the Efficiency of Retirement Savings in Canada” (2018). Link

Healthcare of Ontario Pension Plan, “2021 Canadian Retirement Survey” (2021). Link

Andrew joined the CAAT Pension Plan in 2020, where he is currently Vice President, Strategic Risk Management. Andrew leads a team of pension professionals that combine a deep expertise in funding, plan sustainability and risk management with innovative problem solving.Prior to joining CAAT, Andrew was a Principal at Mercer where he was considered a Canadian expert on pension risk management, asset liability modelling and public sector pension plans. In addition, he spent 2 years at a large Canadian life insurer where he was responsible for actuarial governance and pricing oversight for a full range of group retirement products.

Andrew has spent his career helping Canadian defined benefit pension plans achieve their unique risk management objectives through risk assessment, management, and reduction, and integrating these objectives within their strategy.

Andrew is also an active contributor to the actuarial profession, volunteering on various committees of the Society of Actuaries and Canadian Institute of Actuaries. Andrew graduated from Queen’s University with a Bachelor of Science (Honours). He is a Fellow of the Canadian Institute of Actuaries (FCIA) and a Fellow of the Society of Actuaries (FSA). He is also a Chartered Financial Analyst (CFA) charterholder.